R3 Million Primary Residence Exclusion and Check Higher CGT Exemption Brings Potential Relief

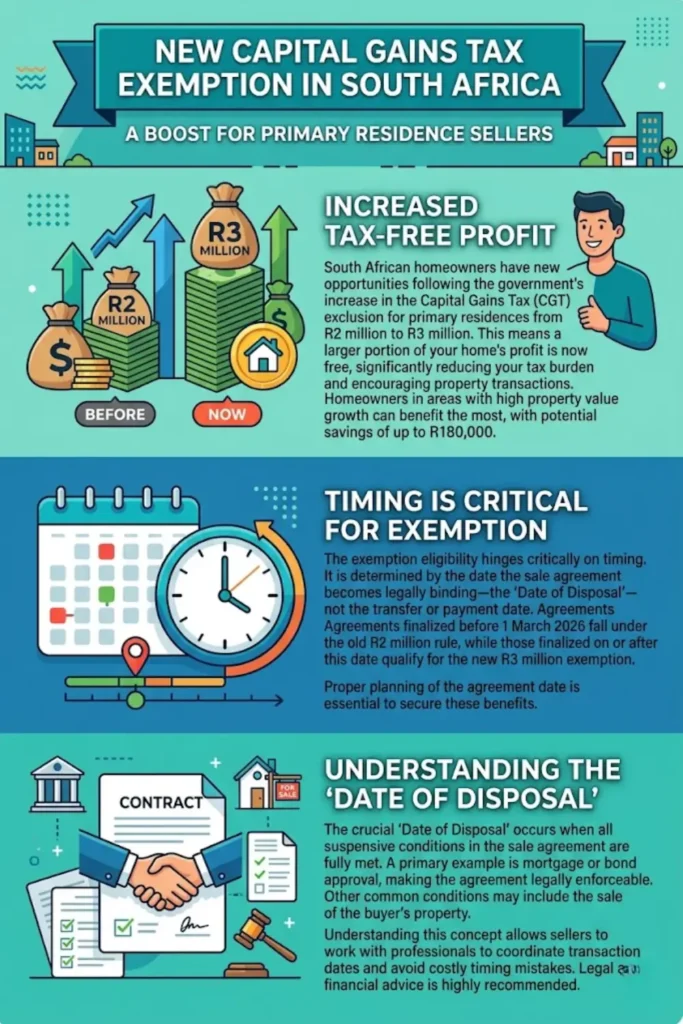

The recent increase in the Capital Gains Tax (CGT) exemption for primary residences in South Africa has created new opportunities for homeowners. With the exclusion rising from R2 million to R3 million, sellers now have the potential to save significantly on taxes when disposing of their homes. However, this benefit is not automatic it depends heavily on the timing of the sale agreement.

Understanding how and when this new rule applies is essential. Many homeowners may assume they qualify for the higher exemption, only to discover that the legal timing of their transaction disqualifies them. This article explains the change in simple terms and highlights what sellers need to know to avoid missing out.

Understanding the New CGT Exemption

The government has increased the CGT exclusion on the sale of a primary residence from R2 million to R3 million. This means that a larger portion of the profit made from selling a home is now tax-free.

This adjustment is particularly beneficial for homeowners in areas where property values have risen significantly. By increasing the exemption threshold, the government aims to reduce the tax burden and encourage property transactions.

Key highlights of the new exemption:

- Tax-free gain increased from R2 million to R3 million

- Applies only to primary residences

- Can reduce taxable capital gains significantly

- Potential tax savings can reach up to R180,000

You can also read: NSFAS Application Center In Kwazulu-Natal

Why Timing Matters in Property Sales

One of the most critical aspects of this tax change is timing. The exemption you qualify for depends on when the sale becomes legally binding not when the money is received or when ownership is transferred.

This means that even if a property is transferred after the new rule takes effect, the old exemption may still apply if the agreement was finalized earlier. Many sellers overlook this detail, which can lead to unexpected tax liabilities.

Important timing considerations:

- Agreements finalized before 1 March 2026 fall under the old R2 million rule

- Agreements finalized on or after this date qualify for the R3 million exemption

- Transfer and payment dates do not affect the exemption eligibility

What Is the “Date of Disposal”?

The “date of disposal” is a key concept in determining which CGT exemption applies. It refers to the moment when the sale agreement becomes fully enforceable by law.

In most cases, this happens when all suspensive conditions are met. A common example is when the buyer’s home loan is approved. Until these conditions are satisfied, the agreement is not legally binding.

Examples of suspensive conditions include:

- Mortgage or bond approval

- Sale of the buyer’s existing property

- Compliance with specific contractual requirements

Understanding this concept helps sellers plan their transactions more effectively and avoid costly mistakes.

You can also read: Who Qualifies for NSFAS Allowances

Financial Impact on Homeowners

The difference between the two exemption thresholds can have a significant financial impact. Even a small change in timing can determine whether part of the profit is taxed or fully exempt.

For example, consider a property sold with a profit of R2.5 million. The applicable exemption will directly affect the taxable amount.

| Scenario | Exemption Applied | Taxable Amount | Result |

|---|---|---|---|

| Agreement before March 2026 | R2 million | R500,000 | Partial tax liability |

| Agreement on/after March 2026 | R3 million | R0 | Fully tax-free gain |

This comparison shows how proper timing can completely eliminate a tax obligation.

Practical Tips for Sellers

To make the most of the new CGT exemption, homeowners need to approach property sales strategically. Being informed and proactive can help maximize savings.

Tips to consider:

- Review your sale agreement carefully before signing

- Understand all suspensive conditions and their timelines

- Coordinate with legal and property professionals

- Plan the transaction date to align with the new exemption

- Keep accurate records of agreement milestones

Taking these steps can help ensure that you benefit from the higher exemption rather than missing out due to technicalities.

Awareness Gaps and Common Mistakes

Despite the significance of this change, not all sellers and agents are fully aware of its implications. The update was not widely highlighted, which has led to confusion in the property market.

Many people mistakenly believe that the transfer date determines the tax exemption. Others fail to consider how delays in meeting conditions can shift the legal date of disposal.

Common mistakes include:

- Assuming transfer date determines CGT exemption

- Ignoring the importance of suspensive conditions

- Finalizing agreements without tax planning

- Relying on outdated information

Avoiding these errors requires a clear understanding of the rules and careful planning.

You can also read: SRD SASSA Status Check 2026

Conclusion

The increase in the CGT exemption to R3 million offers meaningful financial relief for South African homeowners. However, the benefit is not guaranteed it depends entirely on when the sale agreement becomes legally binding.

By understanding the concept of the date of disposal and paying close attention to timing, sellers can maximize their tax savings. A well-timed transaction can mean the difference between paying significant tax and enjoying a completely tax-free gain.